Every time you use a detergent, apply a skincare product, or even take certain medicines, there’s a chance something from Indo Amines was involved. Its chemicals aren’t visible to most of us, but they’re everywhere; in pharma, paints, dyes, flavours, agro products, and even electronics. For a long time, Indo Amines focused on just making these building blocks well. But in 2025, it’s turning the page.

The company is entering a new phase. A large specialty chemicals plant is coming online. It has launched new global-grade products. And it’s showing up in industry circles as a serious player. Without making noise, Indo Amines is steadily moving from being just a dependable supplier to a more forward-leaning innovator in India’s chemical landscape.

By the numbers:

- Market cap: ₹1,074 crore

- FY25 revenue: ₹1,079 crore

- FY25 net profit: ₹56 crore

What’s working?

Indo Amines has deep experience in making aliphatic amines i.e. basic chemical compounds used to manufacture dyes, drugs, paints and cleaning agents. But what’s working now is its ability to add more value. Products are getting more complex. Demand is shifting towards blends that require process innovation. Indo Amines is catching that shift by launching higher-end offerings like Morpholine and its derivatives, which are now being exported to Asia, Europe, and the US.

It also stayed financially disciplined. Margins have remained stable even as costs have gone up in the global supply chain. Profit is up 37% in FY25. Cash from operations is now higher than its reported profits. And that helped fund growth without piling on debt.

New bets

The company’s ₹60 crore plant is a big one. It’s designed for specialty chemicals with tighter quality specs and more demanding industrial buyers. Indo Amines has also picked up industrial land across Maharashtra, signalling more plants are likely to follow. The company’s R&D centre is government-recognised and has 20+ chemists working on custom formulations many of which are tailored to sectors like water treatment, home care, and pharma.

At the June 2025 NextGen Chemicals Summit, Indo Amines presented new use cases around eco-friendly surfactants and personal care intermediates, hinting that it wants to become a more strategic supplier, not just a bulk one.

On-ground execution

Ten factories, a customer base across 40 countries, and high-capacity utilisation: this is a company with operational depth. In FY25, its operating profits crossed ₹100 crore for the first time. Even more telling: its share price moved above long-term technical resistance this June and saw strong buying interest. Meanwhile, promoter stake increased slightly last quarter, a small but notable sign of internal confidence.

What’s not working

A few things could hold it back. Its cash conversion cycle has stretched to 96 days; meaning it takes longer to turn raw materials into revenue and eventually into cash. Payment delays from customers are part of that. Inventory is also taking slightly longer to clear. This ties up capital and limits flexibility.

And while its profit growth is solid, revenue growth over the last year has been more modest. If the new capacity doesn’t translate into faster sales growth in FY26, it could raise questions. The valuation, too, isn’t cheap. It trades at ~19x earnings, slightly ahead of some peers in the segment.

Strategic takeaway

Indo Amines isn’t chasing anyone. It’s doing the slower, harder work of moving up the value chain; launching export-quality molecules, expanding responsibly, and building long-term relevance in the chemicals industry. It’s the kind of story that compounds quietly; until one day, it doesn’t.

Final pour

Not every company needs a dramatic pivot to matter. Indo Amines is betting that execution, scale, and smart product choices are enough to win. And in a world where chemicals are touching more parts of our lives than ever before, that may be all it needs.

FAQs

What does Indo Amines Ltd manufacture?

Indo Amines produces specialty, fine, and performance chemicals used in pharmaceuticals, detergents, dyes, agrochemicals, and personal care products.

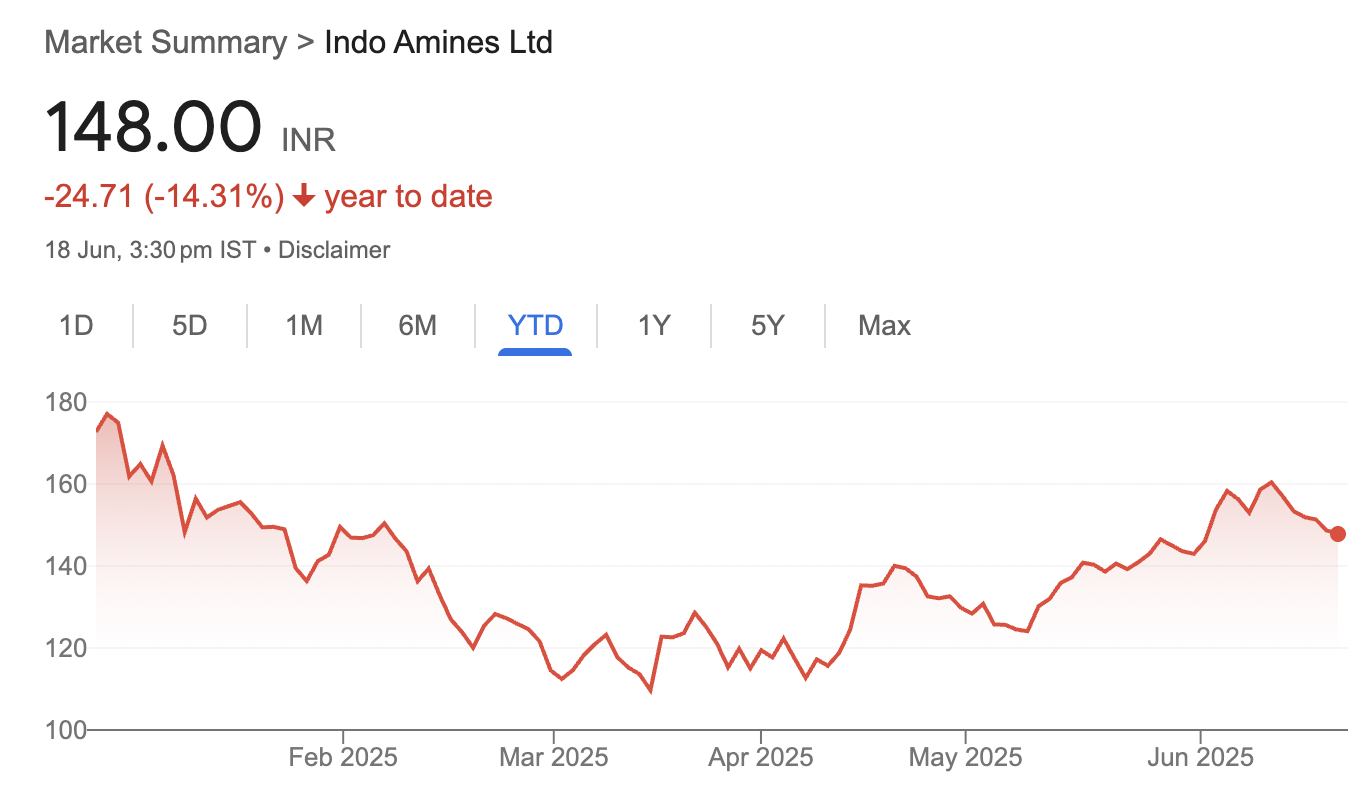

Why has Indo Amines stock fallen in 2025?

Despite operational growth, the stock is down 15% due to modest revenue growth, a stretched cash conversion cycle, and concerns around valuation.

What are aliphatic amines used for?

Aliphatic amines are chemical compounds used in the manufacturing of paints, cleaning agents, drugs, and dyes, serving as key intermediates in various industries.

What is Indo Amines’ new plant focused on?

The new ₹60 crore plant focuses on specialty chemicals with high-quality specifications aimed at global and industrial markets.

Has Indo Amines expanded globally?

Yes, Indo Amines exports to over 40 countries and recently launched Morpholine derivatives for markets in Asia, Europe, and the US.

How profitable is Indo Amines?

In FY25, Indo Amines posted a net profit of ₹56 crore with stable operating margins of around 9% and strong cash from operations.

What is the role of Indo Amines’ R&D centre?

The R&D centre develops custom chemical formulations tailored for sectors like water treatment, pharma, and personal care.

Is Indo Amines investing in green chemistry?

Yes, the company is exploring eco-friendly surfactants and sustainable chemical blends showcased at the 2025 NextGen Chemicals Summit.

What are the risks facing Indo Amines?

Key risks include a stretched working capital cycle, modest revenue growth, and relatively high valuation compared to peers.

What makes Indo Amines worth tracking?

Its disciplined expansion, product innovation, and push into global specialty chemicals make it a quiet but credible long-term growth story.